Use these links to rapidly review the document

QUICKLOGIC CORPORATION TABLE OF CONTENTS

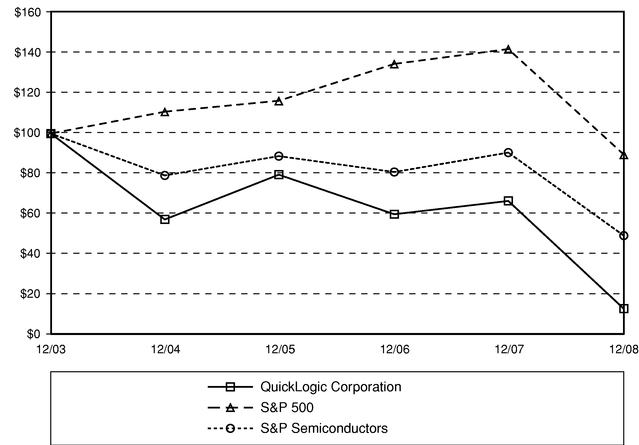

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

FOR THE FISCAL YEAR ENDED DECEMBER 28, 2008 |

||

OR |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to |

||

Commission File Number: 000-22671

QUICKLOGIC CORPORATION

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

77-0188504 (I.R.S. Employer Identification Number) |

|

1277 Orleans Drive Sunnyvale, CA 94089 (Address of principal executive offices, including zip code) |

||

Registrant's telephone number, including area code: (408) 990-4000 |

||

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of Exchange on which Registered | |

|---|---|---|

| Common Stock, $0.001 par value | The NASDAQ Stock Market LLC |

Rights to Purchase Series A Junior Participating Preferred Stock

Securities registered pursuant to Section 12(g) of the Act: None

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer ý | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller Reporting Company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o No ý

The aggregate market value of voting stock held by non-affiliates of the registrant as of June 29, 2008, the Registrant's most recently completed second fiscal quarter, was $51,180,000 based upon the last sales price reported for such date on the Nasdaq Global Market. For purposes of this disclosure, shares of common stock held by persons who hold more than 5% of the outstanding shares of common stock and shares held by executive officers and directors of the registrant have been excluded in that such persons may be deemed to be affiliates. This determination is not necessarily conclusive.

At February 23, 2009, the Registrant had 29,909,393 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Items 10, 11, 12, 13 and 14 of Part III of this Form 10-K incorporate information by reference from the Proxy Statement for the Registrant's Annual Meeting of Stockholders to be held on or about April 22, 2009.

QUICKLOGIC CORPORATION

TABLE OF CONTENTS

2

This Annual Report on Form 10-K contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, that involve risks and uncertainties, as well as assumptions that, if they do not fully materialize or prove incorrect, could cause the business and results of operations of QuickLogic Corporation ("QuickLogic," the "Company,""we", "us" or "our") to differ materially from those expressed or implied by such forward-looking statements. Such forward-looking statements include, without limitation, any projections of earnings, revenue or financial items, any statements of the plans, strategies and objectives of management for future operations, any statements concerning proposed new products, any statements regarding future economic conditions or performance, any statements relating to our projected capital expenditures, any statements of belief and any statements of assumptions underlying the foregoing.

The risks, uncertainties and assumptions referred to above that could cause our results to differ materially from the results expressed or implied by such forward-looking statements include, but are not limited to, those discussed under the heading "Risk Factors" in Item 1A hereto and the risks, uncertainties and assumptions discussed from time to time in our other public filings and public announcements. All forward-looking statements included in this document are based on information available to us as of the date hereof and we assume no obligation to update these forward-looking statements.

Overview

QuickLogic Corporation was founded in 1988 and reincorporated in Delaware in 1999. We develop and market low power customizable semiconductor solutions that enable customers to add features to their mobile, prosumer (PROfessional conSUMER), consumer and industrial products. We are a fabless semiconductor company that operates in a single industry segment where we design, market and support primarily Customer Specific Standard Products, or CSSPs, and, secondarily, Field Programmable Gate Arrays, or FPGAs, associated design software and programming hardware. Our CSSPs are customized semiconductor building blocks created from our new solution platforms including ArcticLink® II, ArcticLink, PolarPro® II, PolarPro, Eclipse™ II and QuickPCI® II (all of which fall into our new product category); our mature product family includes pASIC® 3, QuickRAM®, Eclipse, and EclipsePlus, as well as royalty revenue, programming hardware and design software; our end-of-life product family includes pASIC 1, pASIC 2, V3, QuickMIPS, QuickPCI and QuickFC.

CSSPs are complete, customer-specific solutions that include a unique combination of our silicon solution platform, proven system blocks, or PSBs, custom logic and software drivers. All of our solution platforms are standard silicon products and must be programmed to be effective in a system. Our PSBs range from intellectual property, or IP, which improves video streams to IP which implement commonly used mobile system interfaces, such as Secure Digital Input Output, or SDIO, or Universal Serial Bus 2.0 On-The-Go, or USB 2.0 OTG, to IP that accelerates sideloading speeds in mobile devices. We provide complete solutions by first architecting the solution jointly with our customer's engineering group, selecting the appropriate solution platform and PSBs, providing custom logic, integrating the logic, programming the device and providing software drivers required for the customers' application.

CSSPs, which we pioneered and introduced in the first quarter of 2007, are developed for specific power sensitive applications that have differentiated features in terms of IP, intelligent data processing or connectivity requirements. Target customers value CSSPs for the ability to provide a range of products from a single platform and the flexibility to address specific product requirements or changes. Market leading original equipment manufacturers, or OEMs, and original design manufacturers, or ODMs, seek to develop product platforms from which several products, or SKUs, can be introduced.

3

For example, Mobile Internet Device (MID) companies may plan to introduce products offering mobile TV, WiMAX, HSxPA, Bluetooth 2.x + EDR and USB 2.0 OTG. These customers value our ability to provide a range of CSSPs from a single platform design by incorporating different features in the programmable fabric of our solution platforms. Other customers value the flexibility of programmable fabric to address specific product requirements. By providing customized solutions for these customers we increase their ability to meet the time-to-market and time-in-market pressures associated with their markets.

Although the semiconductor industry as a whole is expected to decline in 2009 with modest growth in 2010, consumer products are a strong driver for semiconductor sales, and the needs of the consumer market have a unique set of requirements. One important trend in the consumer market is towards mobile, handheld devices. The market for mobile, handheld devices is large. In 2008, more than 1.2 billion cellular phones, ranging from multimedia to ultra low cost phones, were sold (according to iSuppli, a market intelligence company). More importantly, iSuppli predicts that the smartphone segment of the overall cellular phone segment will increase 62% over the next three years, from 219 million units in 2008 to 356 million units, by the end of 2011. In fact, the smartphone segment is predicted to be one of the higher growth segments during the current economic downturn.

Other important industry trends affecting the large market for mobile devices include the use of platforms to enable rapid product proliferation, the need for high bandwidth solutions enabling mobile Internet and streaming video, miniaturization and the need to increase battery life. Another important trend is shrinking product life cycles, which drives a need for faster, lower risk product development. There is intense pressure on the total product cost of these devices, including per unit component costs and non-recurring development costs. As more people experience the advantages of a mobile lifestyle at home, they demand the same advantages in their professional lives, and while they are "on the go", or mobile. Therefore, we believe that these trends toward mobile, handheld products which have a small form factor and maximize battery life will also be evident in other segments such as industrial, medical and military.

In addition to CSSPs, we sell products to industrial, military and other customers who do their own selection and integration of IP cores and add software drivers to their application. We market FPGAs, IP cores and software drivers to these customers, who value the low power consumption, reduced development risk through the use of proven IP cores, fast time-to-market, high IP security, instant-on and reliability of our devices.

This range of offerings allows customers to acquire a solution tailored for their needs. Mobile product OEMs and ODMs tend to prefer a complete solution, and purchase CSSPs. Other customers in the industrial or military segments with proprietary IP requirements choose to purchase our FPGAs or ArcticLink II / ArcticLink / PolarPro II / PolarPro solution platforms and utilize our IP cores as appropriate. Whether a customer uses our CSSPs as a complete solution, or proven IP cores with our FPGAs, we believe our solutions and products enable system manufacturers to improve their time-to-market, lower total system power consumption, reduce their development risk and total cost of ownership, and add features or performance to their embedded applications.

Our CSSPs, and the rest of our product offerings, are based on our patented ViaLink® metal-to-metal programmable technology. ViaLink is the foundation of our competitive advantage in providing flexible energy efficient devices and solutions that deliver the high performance, high reliability, IP security and instant-on features that our customers value. In 1991, we introduced our first FPGA products based upon our ViaLink technology. Our ViaLink technology allows us to create devices smaller than our competitors' products on comparable technology, thereby minimizing silicon area and cost. In addition, our ViaLink technology has lower electrical resistance and capacitance than other programmable technologies and therefore supports low power consumption and higher signal speed. Our architecture uses our ViaLink technology to maximize interconnects at every routing wire

4

intersection, which allows more paths between logic cells, and between the hard-wired logic and logic cell portions of our platforms.

We offer a range of CSSPs built on our ArcticLink II VX, ArcticLink, PolarPro II and PolarPro solution platform families. Our PolarPro programmable architecture builds on our low power Eclipse II architecture to provide lower power consumption and a cost effective platform for pure digital applications. During 2008, we introduced the latest addition to the PolarPro solution platform family, called PolarPro II. The PolarPro II solution platform augments the PolarPro family by providing a platform that increases our logic capacity for building CSSPs, and at the same time, further reduces our standby power consumption, reduces our package size, and reduces our manufacturing costs. CSSPs developed using our PolarPro II and PolarPro solution platforms implement PSBs and custom logic in programmable fabric. Based on our engineering analysis of portable, battery powered applications, we believe designers using either PolarPro II or PolarPro can extend battery life by as much as four times as compared to a standard product implementation, setting a new standard for low power consumption through the use of programmable logic.

We started shipping CSSPs based on our ArcticLink solution platform in 2007, and announced a new ArcticLink II VX solution platform in 2008. ArcticLink and ArcticLink II VX solution platforms combine mixed signal physical layers, hard-wired logic and programmable fabric on one device. Mixed signal capability supports the trend toward high-speed serial connectivity in mobile applications, where designers benefit from lower pin counts, simplified printed circuit board, or PCB, layout, simplified PCB interconnect and reduced signal noise. Adding hard-wired intellectual property enables us to deliver more logic per die area, while the programmable fabric allows us to provide CSSPs that can be rapidly customized to differentiate customer products, add features and reduce system development costs. For example, smartphone companies may plan to introduce products offering mobile TV, WiMAX, HSxPA, Bluetooth 2.x + EDR and USB 2.0 OTG. These manufacturers value our solution platforms, since the programmable fabric can be used to implement various combinations of these features into a range of their products from a single platform design.

Our CSSPs provide:

5

We are marketing CSSPs to OEMs and ODMs offering differentiated mobile products. Our target mobile markets include:

Examples of how existing and potential customers benefit from CSSPs are:

Our new products are also being designed into applications in our traditional markets, such as data communications, instrumentation and test and military-aerospace, where customers value the low power consumption, instant-on, IP security, reliability and fast time-to-market of our products.

In addition to working directly with our customers, we partner with other companies that are experts in certain technologies to develop additional intellectual property, reference platforms and system software to provide application solutions. For instance, we licensed elements of VEE from Apical Limited, a U.K. company that sells enhanced video image capability. We also work with mobile processor manufacturers, and companies that supply storage, networking or graphics components for embedded systems. The depth of these relationships varies depending on the partner and the dynamics

6

of the end market being targeted, but is typically a co-marketing program that includes joint account calls, promotional activities and/or engineering collaboration and developments, such as reference designs.

Our headquarters are located at 1277 Orleans Drive, Sunnyvale, California 94089. We can be reached at (408) 990-4000, and our website address is www.quicklogic.com. Our common stock trades on the Nasdaq Global Market under the symbol "QUIK". Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to such reports are available, free of charge, on our Internet home page as soon as reasonably practicable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission, or SEC. Copies of the materials filed by the Company with the SEC are also available at the Public Reference Room at 100 F Street, N.E., Washington, D.C., 20549. Information regarding the operation of the Public Reference Room is available by calling the SEC at 1-800-SEC-0330. Reports, proxy and information statements and other information regarding issues that we file electronically with the SEC are available on the SEC's website at www.sec.gov.

In addition, information regarding our corporate governance guidelines, code of conduct and ethics guidelines and the charters of our Audit, Compensation and Nominating and Corporate Governance Committees are available free of charge on our website noted above.

Product Technology

Our product technology consists of four major elements.

First, our patented ViaLink metal-to-metal programmable technology is the foundation of our competitive advantage in providing flexible, energy efficient devices and solutions that deliver high performance, high reliability, intellectual property security and instant-on features that our customers value. Unlike other programmable technologies, ViaLink uses metallurgical changes in amorphous silicon to complete connections. In particular, an unprogrammed ViaLink uses amorphous silicon to separate two conductors. When mixed with a metal such as tungsten or titanium, amorphous silicon can be turned into a silicide, which is a good conductor providing very low resistance in a 'closed' ViaLink. During programming, we use an electrical voltage to create the silicide and selectively 'close' the desired ViaLink connections. Along with the advantages of low leakage and low resistance, this metallurgical change is permanent with 'instant-on' characteristics that are not susceptible to 'single event upsets' or 'brownout' conditions. Also, the fact that the silicide is low resistance means that only a small amount is required and, as a result, our ViaLink connections are very small, which translates into reduced silicon area, low parasitic capacitance and excellent routability, all of which contribute to high performance at low power and low cost relative to SRAM and flash based FPGA technologies. We developed our proprietary programmable logic architecture to take advantage of the unique strengths of the ViaLink technology.

We believe that the underlying attributes of our ViaLink technology include:

7

Second, our ArcticLink solution platform combines mixed signal physical layers, hard-wired logic and programmable logic on one device. Mixed signal capability supports the trend toward serial connectivity in mobile applications, where designers benefit from lower pin counts, simplified PCB layout, simplified PCB interconnect and reduced signal noise. Adding hard-wired intellectual property enables us to deliver more logic at lower cost and lower power; while the programmable logic allows us to provide solutions that can be rapidly customized to differentiate products, add features and reduce system development costs. This combination of mixed signal, hard-wired logic and programmable logic enables us to deliver low cost, small form factor solutions that can be customized for particular customer or market requirements while lowering the total cost of ownership. The high routing density and flexibility of our ViaLink technology is critical to the efficient interface between the hard-wired logic and the programmable fabric.

Third, we develop and integrate PSBs which are innovative IP cores, intelligent data processing IP cores, or standard interfaces used in mobile products. We offer:

Our recently announced Smart Programmable Integrated Data Aggregator, or SPIDA, technology—is able to intelligently move data between peripherals without significant involvement from the application processor, thereby reducing processor loading and system power consumption.

Lastly, our CSSPs are complete solutions that we develop for target customers who wish to bring differentiated, mobile products to market quickly and cost effectively. We partner with customers to define solutions specific to their requirements, and combine all of the above technologies—one of our PolarPro II, PolarPro, ArcticLink II or ArcticLink solution platforms, PSBs, which are proven logic IP cores, custom logic and software drivers. We then work with these customers to integrate and test CSSPs in their systems. The benefit of providing complete solutions is that we effectively become a virtual extension of our customers' engineering organization.

Industry Background

Consumer Electronic (CE) products are a strong growth market for semiconductor sales, and the needs of this market bring a unique set of requirements. One important trend in this market is toward mobile, handheld devices with wireless capability. Important industry trends affecting the large market for mobile devices include the need for high bandwidth that enables the same user experience consumers are accustomed to on the personal computer (PC), such as Internet browsing, social networking and streaming video, product miniaturization and the need to increase battery life. Many of these product requirements were driven from the launch and widely publicized success of the Apple iPhone. Furthermore, while there continues to be additional deployments in the network operator infrastructure that supports the bandwidth required for the aforementioned use cases, there are demographical and geographical nuances for specific product features that share this infrastructure. These nuances put a burden on the designers and manufactures of these mobile CE products as they try to tailor multiple products with limited engineering resources. Lastly, the fast pace at which the

8

consumer taste for these features changes exacerbates the development challenges and risk in launching successful products to the marketplace.

Another important trend is shrinking product life cycles, which drives a need for faster, lower risk product development. There is intense pressure on the total BOM cost of these devices, including per unit component costs and non-recurring development costs. As more people experience the advantages of a mobile lifestyle at home, they demand the same advantages in their professional lives. Therefore, we believe that these trends toward mobile, handheld products which have a PC-like user experience, small form factor and maximize battery life will also be evident in the computing, industrial, medical and military markets. One such example is the trend of Notebook and Laptop makers to come out with the new, smaller form factor Netbook.

These industry trends are shifting the demand among different classes of core silicon. The three main classes of core silicon are:

ASSP use is largely driven by the adoption of industry standards that have been developed to address increasing system complexity and the need for communication between systems and system components. These standards include:

ASSPs offer the system designer proven functionality which reduces development time, risk and cost. However, since these devices are offered broadly to the market, it is challenging for a system designer to create differentiated products from these devices alone. Furthermore, in many situations the

9

available ASSPs may not directly implement the desired function, which then requires the system designer to use a combination of ASSPs to achieve the desired result at the expense of increased cost, product size and power consumption. Additionally, as standards evolve or new standards are developed, ASSPs may not be available to implement desired functions. Therefore, many system designers supplement their ASSPs with customizable components such as PLDs or ASICs.

PLDs offer the system designer the ability to create custom functions that either provide product differentiation or make up for deficiencies in available ASSPs. Because PLDs are electrically customized, they can be customized by the designer at his location in minutes and, because blank PLDs are a standard product, lead times are short. PLDs are flexible and can be adapted to address new market requirements. Compared to ASSPs, PLDs require more designer input, since the designer has to develop the IP to go into the specific PLD and may also have to develop the software to drive the IP. The additional designer input increases development time, development cost and development risk relative to an ASSP. However, compared to an ASIC, the programmability of a PLD reduces development time, cost and risk. Also, for any given function, a PLD will have a higher unit cost and consume more power than either an ASSP or an ASIC as the device size required to implement a function in a PLD is larger than that of an ASSP or ASIC. Consequently PLDs have stratified into small PLDs like Complex Programmable Logic Devices, or CPLDs, that are low cost, low power, lower performance and simpler to design due to their small number of logic cells, and FPGAs, which are typically larger and have higher performance and power consumption. The small PLDs are typically used to 'tweak' designs made from a collection of ASSPs, whereas FPGAs are traditionally used to create high value custom designs.

ASICs offer the system designer the ability to create custom functions that have exceptionally low unit cost, low power, small size and high performance. The drawback to an ASIC is the expensive, time consuming and high risk development cycle. As with PLDs, the system designer has to develop the IP and software, and because an ASIC requires its own mask set and production cycle, it is both expensive and slow to manufacture and debug. Thus ASICs tend to be used for high volume designs where the development cost can be offset by unit cost savings realized over a very high volume. While driving down the technology curve, also known as following Moore's Law, has resulted in many benefits for ASICs, it has also created a design challenge. While the dramatic increase in mask costs with each new technology is well known, another factor is that each generation allows us to build far more complex devices, which take more time to define, to design and to debug. Thus development cost, development time and development risk increase with each generation, with the result that the volume required to offset the development cost increases. Unfortunately, it is often the case that a large, complex device can only serve a small number of SKUs, which makes it even harder to achieve the high volumes required to amortize the development costs, and large ASICs cannot be easily adapted to changing market conditions.

System designers can customize their products using either programmable logic or ASICs, and the competitive dynamic between these classes of core silicon are well understood. The high development risk and cost and the opportunity cost of an ASIC is incurred to produce custom devices with a very low unit production cost. Suppliers of programmable logic devices, which have lower development risk, development cost and market risk relative to ASICs, have aggressively reduced the unit cost of their products over time, making programmable logic devices the solution of choice for custom products unless the volume is very high. These cost reduction efforts have significantly increased the volume needed to justify the total cost of an ASIC.

The consumer market, especially the mobile device market, is not well served by mainstream core silicon. Consumer devices incorporate complex, rapidly changing technology, require rapid product proliferation, and have short product life cycles and short development cycles. Therefore, most mobile designers design their products from a base platform, or reference design, provided to them by the vendor of the processor they have selected for their design. To differentiate the OEMs/ODMs products

10

from competition, some level of customization may be required at either the hardware or software level. Designers have only a few viable options to modify the base platform for their needs. Since mobile system designers require very low power consumption to maximize battery life in their applications, the high power consumption of FPGAs is incompatible with their design goals. Thus, the average mobile system designer is effectively limited to ASSPs and small PLDs, which creates a virtually level playing field among mobile system designers, and makes product proliferation and differentiation extremely hard to achieve. ASICs—with their long development cycles, long lead times and high non-recurring development costs—are only used in very high volume mainstream consumer products.

Aside from the consumer market, however, the traditional military and industrial markets are well served by existing core silicon. Much of this market uses complex ASSPs since price, power and size are not particularly critical design considerations. When there is a strong need for a custom solution in high volume applications, designers turn to an ASIC and, in low to medium volume applications, they use FPGAs. QuickLogic FPGAs have a loyal following in certain segments of these markets, particularly when instant-on, energy efficiency, high reliability or intellectual property security is important. These markets are expected to continue to grow, but not as significantly as the consumer market.

QuickLogic's Solutions

We market CSSPs to mobile device OEMs and ODMs. CSSPs are complete solutions incorporating our ArcticLink II VX, ArcticLink, PolarPro II or PolarPro solution platforms, packaging, PSBs, custom logic, software drivers, and our architecture consulting. We partner with target customers' in our focus markets to architect and design CSSPs, and integrate and test them in our customers' products. A CSSP is based on our programmable technology, which enables customized designs, low power, flexibility, rapid time-to-market, longer time-in-market and lower total cost of ownership. From a mobile system designer's perspective, a CSSPs function is known and complete, and can consequently be designed into systems with a minimum amount of effort and risk. One of the features of our ViaLink technology is that it is non-volatile, which means that we can program a CSSP in our factory, and then ship it fully configured to a customer. To that customer, our solution looks exactly like a custom ASSP. We are capable of providing complete solutions because of our investment in developing the low power PSBs and software required to implement specific functions. Furthermore, because we are involved with our customers at the definition stage of their product, we are able to architect solutions that typically have more than one PSB, absorbing more functionality traditionally implemented with multiple ASSPs. In cases where our CSSP has multiple PSBs, significant system performance or battery life improvements can be realized by enabling direct data transfers between the PSBs. QuickLogic refers to this layer of functionality as SPIDA (Smart Peripheral Integrated Data Aggregator) technology. In some cases, we develop the PSBs and software ourselves and, in other cases, we utilize third parties to develop the mixed signal physical layers, logic and/or software.

We market CSSPs to customers in trouble mode, where they have an immediate need to address, and to customers in growth mode, where CSSPs are used as a platform to develop differentiated mobile products. For example, a broadband data card customer in trouble mode needed an immediate change to their system design. This customer was trying to quickly respond to a significant change in the end market requirements for data cards by integrating additional flash memory using an interface that was not included in the main modem chipset. We developed a CSSP using the ArcticLink solution platform that enabled this manufacturer to integrate this new flash memory, as well as support the SPIDA capability needed for high performance USB-to-SD transfers, commonly known as "sideloading" in the consumer market. The flexible features of our programmable fabric allowed us to develop a complete solution using standard product silicon and allowed our customer to increase their served available market (SAM) for their devices.

11

In a growth mode example, a smartphone customer selected a PolarPro CSSP, so that they could integrate additional wireless technology into their product, without having to change their base platform. By augmenting their existing platform and processor, they were able to leverage all of their existing developments, software, and architecture expertise while still addressing emerging requirements for multiple wireless radios in a single smartphone.

Our sales cycle for trouble mode opportunities is typically 9 to 12 months, and is typically 9 to 18 months for growth mode opportunities. Growth mode opportunities provide us early interaction with system architects about the challenges they face, which gives us better insight into trends and future needs. This insight has proved invaluable as we define and execute our PSB and solution platform roadmap strategy.

Our ViaLink technology is inherently the lowest power programmable technology used to design programmable logic. As a result, we have focused our product and marketing efforts on the mobile device market, where battery life is critical. The fact that we use our programmable technology to customize these CSSPs provides two advantages over conventional ASSPs that are based on ASIC technology. Foremost is the fact that our CSSPs can be tailored for a specific customer's requirements. Once we have developed proven system blocks, it is easy to combine PSBs and utilize the remaining programmable logic to provide a unique set of features to a mobile system designer, or to add other functions to the CSSP, such as UARTs, keyboard scanning functions, and SPI ports, which minimizes system size and cost. We are able to develop these CSSPs from a common solution platform, and partner with system designers to implement a range of solutions, or products, that address different geographic and market requirements. Finally, by using programmable technology instead of ASIC technology, we reduce the development time, development risk and total cost of ownership and are able to bring solutions to market far quicker than other custom silicon alternatives.

FPGAs which are based on SRAM or flash technology are not well suited to implementing CSSPs for the mobile device market. These conventional programmable logic architectures consume more power, especially in standby mode, which makes them unsuitable for battery powered devices. They may also require a separate configuration memory, which increases the total size and cost of the solution. Finally, SRAM based programmable logic is not 'instant-on', which significantly complicates system design, increases power consumption and typically results in increased development time, risk and cost.

By using CSSPs, proven system blocks, in-depth architecture knowledge, and ViaLink as core technologies, we can deliver energy efficient custom solutions that blend the benefits of traditional ASSPs with the flexibility, product proliferation, differentiation and low total cost of ownership advantages of programmable logic.

Our System Solutions Group, or SSG, is our internal group that provides system architecture and design services to create CSSPs for our customers. When a mobile system designer requires a high value, complex solution that is unlike any of the CSSPs that we already offer, it can engage with our SSG to develop a platform or solution that meets its specific needs. For instance, we engaged with a wireless hard disk drive OEM where our CSSP allows for the intelligent transfer of data, which improves the data transfer rate, virtually eliminates the CPU cycles associated with data transfer and improves battery life. In this product, the mobile system designer is the primary source of application knowledge and we provide the complex logic and low power design knowledge. In fact, the initial concept and implementation of the SPIDA PSB stemmed from this customer engagement. From the customer's perspective, this is very different from the ASIC model since we develop their CSSP on our existing solution platform, which is a standard product with programmable logic, and does not have the high NRE, tooling expense or inventory and development risk associated with ASIC wafer fabrication. In effect, we produce an energy and cost-efficient custom solution with significantly reduced development and debug time, risk and cost.

12

The QuickLogic Strategy

Our objective is to empower mobile market leaders to achieve mass customization with innovative CSSPs. Market leading companies need to deliver new products quickly and cost effectively. We believe that our patented, proprietary ViaLink technology allows us to deliver customizable, programmable solutions with the lowest power consumption and highest IP security, while meeting system performance and BOM cost requirements. We believe our CSSPs, consisting of our architecture consulting, silicon solution platform, proven and custom system blocks and software drivers, enable OEMs and ODMs to rapidly bring new and differentiated products to market quickly and cost effectively. CSSPs enable energy and cost efficient solutions and enable design platforms from which a range of products can be introduced.

Extend Technology Leadership

We introduced CSSPs in the first quarter of 2007. We had CSSP revenue of $2.9 million and $6.2 million in 2007 and 2008, respectively. We intend to extend our technology leadership by expanding our CSSP capability through the development of additional proven system blocks with innovative or new functionality, the introduction of new solution platforms, and the introduction of smaller form factor packaging technology.

Our CSSPs are based on combinations of our ArcticLink II VX, ArcticLink, PolarPro II and PolarPro solution platforms, and proven system blocks (PSBs). Our design strategy is to combine mixed signal physical layers, hard-wired logic and programmable fabric on one device. Mixed signal capability supports the trend toward serial connectivity in mobile applications, where designers benefit from lower pin counts, simplified PCB layout, simplified PCB interconnect and reduced signal noise. Adding hard-wired intellectual property enables us to deliver more logic in a given die area, while the programmable fabric allows us to provide CSSPs that can be rapidly customized to differentiate products, add features and reduce system development costs. Market leading companies seek to develop product platforms from which several products can be introduced. This combination of mixed signal physical layer, hard-wired logic and programmable fabric enables us to deliver low cost, small form factor solutions that can be customized for particular customer or market requirements.

In March 2008, we announced our ArcticLink II VX solution platform family, consisting of three variants, VX1, VX2 and VX3. All three of these platforms contain the VEE PSB, among other functions. The VX1 solution platform includes VEE with programmable fabric, tailored for applications that use a typical RGB type display and a mobile processor with an RGB output to a display. The VX1 supports up to wide VGA resolution displays. The VX2 solution platform is similar to VX1, but also supports higher resolution displays—up to Wide XGA. The VX3 solution platform includes all of the features of VX2, as well as a MIPI host PSB that allows for connection to MIPI-based displays—an emerging type of display for the mobile market.

In May 2008, we announced a new Wafer Level Chip Scale Package (WLCSP) for the ArcticLink solution platform. Addressing the needs of the mobile space to optimize the I/O per square millimeter of PCB material, this new WLCSP technology eliminates the area overhead of conventional BGA packaging and it is done with a standard die by fabricating an additional metal redistribution layer to re-route the I/O lines from the perimeter bonding pads to an array of balls. It then "bumps" (adds solder balls to) the array, making it ready for OEMs and ODMs to use in conventional surface-mount fabrication processes. The ArcticLink solution platform was initially launched in June 2007, and combines a mixed signal USB physical layer, USB 2.0 OTG and SD/SDIO/CE-ATA in hard wired logic with ViaLink programmable fabric. We continue to develop additional CSSPs from our ArcticLink solution platform, pointing to the inherent value of the programmable fabric in our solution platforms. Without the on-board programmable fabric, we would need to create a new device for these iterations.

13

In December 2008, we announced a new PSB called EBI2, which when coupled with our VEE PSB, allows OEMs and ODMs to easily adopt the VEE technology into handsets using Qualcomm's mobile chipsets and EBI2-based displays. EBI2-based displays are commonly used in handsets with displays that support resolutions between Quarter VGA (QVGA) and Wide QVGA (WQVGA). This new PSB was architected and developed in conjunction with a prominent OEM in the mobile market—underscoring the important of having architecture discussions with our customers.

We continued to have significant shipment of PolarPro devices in 2008. Our PolarPro and PolarPro II families of solution platforms are low-power, cost effective programmable platforms that we combine with proven system blocks, custom logic and software drivers to provide pure digital CSSPs to our customers. Our PolarPro II and PolarPro solution platforms are energy efficient and were designed with an architecture that meets the interconnect and system logic requirements of power sensitive and portable applications. Both families address the interconnect and logic requirements of power sensitive, portable applications by including embedded circuitry for implementing high bandwidth bus-to-bus interfaces, including large arrays of on-chip dual-port SRAM with co-located asynchronous First-In, First-Out, or FIFO, controllers, DDR interfaces for highly cost effective memory expansion and clock management units. PolarPro II is scheduled to go to mass production status during the first half of 2009. We expect CSSPs that do not require any of the high speed serial, mixed signal PHYs, or VEE technology will be architected using the PolarPro II solution platform beginning in 2009.

We also plan to extend our technology leadership by adding high value proven system blocks for mobile device designs. Our strategy is to bring to market these PSBs and the related software drivers. Several announcements highlight our trend toward value added IP. In March 2008, we announced the VEE, an innovative PSB developed for mobile applications that enables a better user experience through video processing technology that sharpens color and effective contrast ratio while extending battery life. We licensed elements of this IP from Apical Limited, who has been providing video enhancement intellectual property for the digital camera and flat panel display markets.

In 2008 we announced several PSBs, including:

We also develop intelligent data processing proven system blocks and the associated software drivers. Intelligent data processing is the movement of data between peripherals without significant involvement from the application processor. For instance, we worked with a wireless hard disk drive manufacturer to move data from a USB interface into a buffer memory and through a Parallel ATA interface to a hard disk drive. Our solution improves the data transfer rate by approximately one level of magnitude compared to managing this data flow with an application processor, which improves the user experience when downloading video and significantly extends battery life. In 2008, we began adapting this type of data processing PSB for a broadband data card application. In this data card application, our solution improved the data transfer rate between a USB interface to a PC or laptop and a microSD memory embedded in the data card. Using our programmable fabric, we designed a

14

custom direct memory access (DMA) engine and highly tuned local bus interface to the wireless modem to achieve this performance. Both of these types of PSBs fit within our Smart Peripheral Integrated Data Aggregator (SPIDA) category of PSBs that we announced during the first quarter of 2009. We expect to continue bringing to market additional PSBs in this category of PSBs.

Small form factor is a significant consideration for mobile system designers and we address form factor in three primary ways.

We intend to continue our investment in advanced package and programmed die technologies to address the form factor needs of the mobile market.

Provide a Range of Offerings

We recognize that our markets require a range of solutions, and we intend to work with market leading companies to combine silicon solution platforms, PSBs, packaging technology and software drivers to meet the product proliferation, high bandwidth, time-to-market, time-in-market and form factor requirements of mobile device manufacturers. We expect CSSPs to range from devices with mixed signal and visual enhancement capability to devices which reduce BOM costs and simplify PCB layout. We intend to continue to define and implement compelling CSSPs for our target customers.

We have a loyal military, industrial and mobile product customer base that prefers to purchase our silicon products, select and integrate IP and develop software drivers to complete their system designs. We expect to continue to offer silicon devices, IP cores and software design capability to these customers. During 2008, we announced that an additional PolarPro programmable platform, the QL1P1000, was production ready. The QL1P1000 contains one million logic cells and was developed for the industrial and military markets.

Market Leading Customers

As a part of our objective to empower mobile market leaders to achieve mass customization with innovative CSSPs, our business model includes a focused customer strategy in which we target market leading customers, who primarily serve the market for differentiated mobile products. Our belief is that a large majority of our revenue will ultimately come from less than 100 customers as we transition to this business model. We have identified and will continue to identify the customers we want to serve with CSSPs. We are currently in different stages of engagement with a number of these customers. We believe CSSPs, which are customer specific solutions with standard product economics, are resonating with our target customers. These customers value the platform design capability, rapid time-to-market,

15

longer time-in-market and low total cost of ownership available through the use of CSSPs. We expect to partner with top customers to define new silicon solution platforms and proven system blocks.

Cost Effective Products

We have changed our product definition and manufacturing strategies to reduce the cost of our silicon solution platforms to enable their use in high volume, mass customization products. Our PolarPro II and PolarPro solution platforms include an innovative logic cell architecture, which enables us to deliver twice the programmable logic in the same die size. Our ArcticLink II and ArcticLink solution platforms combine mixed signal physical layers and hard-wired logic alongside programmable fabric. Mixed signal capability supports the trend toward serial connectivity in mobile applications, where designers benefit from lower pin counts, PCB layout, simplified PCB interconnect and reduced signal noise. Hard-wired logic is very cost effective and energy efficient and we typically implement sophisticated logic blocks in hard-wired logic for these reasons. ArcticLink II and ArcticLink combine cost effective physical layers and hard-wired logic with the flexibility, time-to-market and time-in-market advantages of programmable logic. We have developed small form factor packages, which are less expensive to manufacture and include smaller pin counts. Reduced pin counts result in lower costs associated with our customer's printed circuit board space and routing. Our ability to sell programmed die as CSSPs greatly reduces our costs, allowing us to participate in high volume opportunities. In addition, we have dramatically reduced the time required to program and test our devices, which has reduced our costs and lowered the capital equipment required to program and test our devices. We expect to continue to invest in silicon solution platforms and manufacturing technologies which make us cost effective for high volume applications.

Strategic Relationships

We partner with intellectual property suppliers, market leaders and key suppliers to expand our served market and speed our time-to-market.

16

depth of these relationships varies depending on the partner and the dynamics of the end market being targeted, but is typically a co-marketing program that includes joint account calls, promotional activities and/or engineering collaboration, such as reference designs.

Create Innovative, Industry Leading System Architecture and Design Services

We provide system architecture, design services and development tools to our customers.

Customers and Markets

A significant portion of our revenue comes from sales to customers located outside of the United States, distributors and key customers. Our two largest customers (Honeywell International Inc. and Garmin Ltd.) each represented 17% of revenue in 2008 and a PND customer represented 11% of our revenue in the fourth quarter of 2008. Please see Note 13 to our consolidated financial statements for information on our revenue by geography, market segment and key customers.

In the past, there has not been a predictable seasonal pattern to our business. However, we may experience seasonal patterns in the future due to global economic conditions, the overall volatility of the semiconductor industry, and the inherent seasonality of the mobile and consumer markets.

Sales and Technical Support

We sell our products through a network of sales managers, independent sales representatives and point-of-sale distributors in North America, Europe and Asia. In addition to our corporate headquarters in Sunnyvale, we have regional sales operations in Texas and Illinois. We also have international sales operations in the United Kingdom, China, Japan, Hong Kong, Taiwan and South Korea. Our sales personnel and independent sales representatives are responsible for sales and application support for a given region, focusing on major strategic accounts.

Our customers typically order our products through our distributors. Distributors also create demand for our devices and solutions, generally focusing on customers who are not directly served by our sales managers. Currently, we have two distributors in North America and a network of 15 distributors throughout Europe and Asia to support our international business. Our distributors work

17

with our regional sales managers in identifying new opportunities for our devices and solutions and providing technical support, along with other value added services.

Backlog

We do not believe that backlog as of any particular date is indicative of future results. A majority of our quarterly shipments are typically booked during the quarter. Our sales are made primarily pursuant to standard purchase orders issued by OEM and distributor customers. Under our standard terms and conditions, a significant portion of our backlog is subject to cancellation or reschedule by these customers. Our distributor backlog is also subject to price adjustments upon the resale of the related inventory, as a result the total value of our backlog is not indicative of the related revenue. We believe that generally only a small portion of our backlog, other than orders received under end-of-life programs, is non-cancelable and that the dollar amount associated with the non-cancelable portion is not significant.

Competition

The semiconductor industry is intensely competitive and characterized by:

We believe that important competitive factors in our market are:

A number of companies offer products that compete with one or more of our products and solutions. Our existing competitors for CSSPs include: (1) suppliers of ASSPs such as Cypress Semiconductor; (2) suppliers of mobile and/or application processors, such as Texas Instruments Inc.; and 3) suppliers of ASICs, such as Winbond and LSI Logic. Our existing competitors for FPGAs include: (1) suppliers of CPLDs, such as Lattice Semiconductor and Altera; (2) suppliers of FPGAs, particularly Xilinx and Actel; and (3) and the ASSP competitors noted above. Xilinx and Altera

18

dominate the programmable logic market and have substantially greater revenue, market presence and financial resources than Actel, Lattice or us. Xilinx dominates the FPGA segment of the market while Altera dominates the CPLD segment of the market. ASSPs offer proven functionality which reduces development time, risk and cost, but it is difficult to offer a differentiated product using standard devices, and ASSPs that meet the system design objectives are not always available. Programmable logic may be used to create custom functions that provide product differentiation or make up for deficiencies in available ASSPs. PLDs require more designer input since the designer has to develop and integrate the IP and may have to develop the software to drive the IP. PLDs are more expensive and consume more power than ASSPs or ASICs, but they offer fast time-to-market and are typically reprogrammable. ASICs have a large development cost and risk and a long time to market. As a result ASICs are generally only used for single designs with very high volumes. CSSPs enable custom functions and system designs with fast time-to-market and longer time-in-market since they are customized by us using our solution platforms that contain programmable logic. In addition, because they are complete solutions, they reduce the system development cost and risk. Finally, CSSPs are very energy efficient as result of our ViaLink technology and how we intelligently architect our PSBs, and are suitable for OEMs or ODMs offering mobile differentiated products. As we introduce additional solutions, we will also face competition from standard product manufacturers who are already servicing or who may decide to enter the markets addressed by our solutions. In addition, we expect significant competition in the future from major domestic and international semiconductor suppliers and from suppliers of products based on new or emerging technologies.

Research and Development

Our future success will depend to a large extent on our ability to rapidly develop, enhance and introduce devices and CSSPs that meet emerging industry standards and satisfy changing customer requirements. We have made and expect to continue to make substantial investments in research and development. In the second quarter of 2008, we established a plan to outsource certain development functions that were previously performed in-house. The change of certain development activities to an on-demand, outsourced model from an in-house, fixed cost model was implemented by the second quarter of 2008.

As of the end of 2008, our research and development staff consisted of 24 employees located in Canada, India and California.

19

Manufacturing

We have close relationships with third party manufacturers for our wafer fabrication, package assembly, testing and programming requirements to help ensure stability in the supply of our products and to allow us to focus our internal efforts on product and solution design and sales.

We currently outsource our wafer manufacturing, primarily to TSMC and Tower. TSMC manufactures our pASIC 3, QuickRAM and certain QuickPCI products using a four-layer metal, 0.35 micron complementary metal oxide semiconductor, or CMOS, process. TSMC also manufactures our Eclipse and other mature products using a five-layer metal, 0.25 micron CMOS process on eight-inch wafers. We purchase products from TSMC, on a purchase order basis.

Tower manufactures our new products, and will manufacture new products currently under development, using a six-layer metal, 0.18 micron CMOS process incorporating our ViaLink technology. We have invested $21.3 million in Tower as part of Tower's efforts to build and equip their wafer fabrication facility. Our investment guarantees us a portion of their available wafer fabrication capacity at competitive pricing. Our Tower agreement provides for guaranteed capacity availability through at least 2010.

Outsourcing of wafer manufacturing enables us to take advantage of these suppliers' high volume economies of scale. We may establish additional foundry relationships as such arrangements become economically useful or technically necessary.

We outsource our product packaging, testing and programming primarily to Amkor Technology, Inc and Unisem (M) Berhard.

Product Revenue Transition

Our business is in transition, besides the global economy condition and competition in semiconductor market, there are two other factors affecting our future growth: increased revenue through the success of our CSSP strategy, which we announced in the first quarter of 2007, and an expected decline in revenue from end-of-life products. CSSP revenue is included in our new product revenue. New products contributed revenue of $1.5 million, or 26% of total revenue, in the fourth quarter of 2008. One customer, purchasing CSSPs in Asia for use in PND products, accounted for 18% of total revenue in the fourth quarter of 2008. We believe CSSPs will result in significant new product growth and total revenue, but we cannot assure investors when this will occur.

We also expect a decline in revenue from our end-of-life products. We announced the end-of-life of certain products for two primary reasons: (1) certain suppliers decided not to renew their agreements to supply us with wafers. For instance, the supplier of wafers for our pASIC 1 and pASIC 2 devices, which were released to production from 1991 through 1997, decided not to renew our supply agreement, and future sales of these devices are limited to inventories on hand; and (2) we decided to end-of-life QuickMIPS and QuickPCI devices so that we could focus our engineering resources on new products. End-of-life products contributed revenue of $808,000, or 14% of total revenue, in the fourth quarter of 2008, and we currently expect these products to contribute less than 10% of our total revenue by the second quarter of 2009.

In order to maintain or grow our revenue from its current level, we are dependent upon increased revenue from our existing products, especially CSSPs utilizing our ArcticLink II, ArcticLink, and PolarPro II, and PolarPro solution platforms, and the development and marketing of additional new products and solutions.

20

Employees

As of December 28, 2008, we had a total of 88 employees worldwide. We believe that our future success will depend in part on our continued ability to attract, hire and retain qualified personnel. None of our employees are represented by a labor union and we believe our employee relations are favorable.

Intellectual Property

Our future success and competitive position depend upon our ability to obtain and maintain the proprietary technology used in our principal products. We hold 99 U.S. patents and have six pending applications for additional U.S. patents containing claims covering various aspects of programmable integrated circuits, programmable interconnect structures and programmable metal devices. In Europe and Asia, we have been granted a total of six patents and have a total of six patent applications pending. Our issued patents expire between 2010 and 2027. We have ten trademarks registered with the U.S. Patent and Trademark Office.

From time to time, we receive letters alleging patent infringement or inviting us to license other parties' patents. We evaluate these requests on a case-by-case basis. Offers such as these may lead to litigation if we reject the opportunity to obtain the license or reject the other party's demands.

Executive Officers and Directors

Our executive officers are appointed by, and serve at the discretion of, our Board of Directors. There are no family relationships among our directors and officers.

The following table sets forth certain information concerning our current executive officers and directors as of February 23, 2009:

Name

|

Age | Position | |||

|---|---|---|---|---|---|

E. Thomas Hart |

67 | Chairman of the Board and Chief Executive Officer | |||

Andrew J. Pease |

58 | President | |||

Terry L. Barrette |

52 | Vice President, Operations | |||

Ajith Dasari |

38 | Vice President, Worldwide Engineering | |||

Brian Faith |

34 | Vice President, Worldwide Marketing | |||

Ralph S. Marimon |

51 | Vice President, Finance and Chief Financial Officer | |||

Catriona Meney |

47 | Vice President, Human Resources and Development | |||

Timothy Saxe |

53 | Senior Vice President, Engineering and Chief Technology Officer | |||

Michael J. Callahan |

73 | Director | |||

Michael R. Farese |

62 | Director | |||

Arturo Krueger |

69 | Director | |||

Christine Russell |

59 | Director | |||

Hide L. Tanigami |

58 | Director | |||

Gary H. Tauss |

54 | Director | |||

E. Thomas Hart will become our Chairman of the Board and Chief Executive Officer effective March 30, 2009 and has served as our President, Chief Executive Officer and a member of our Board of Directors since June 1994, and as our Chairman since April 2001. Prior to joining QuickLogic, Mr. Hart was Vice President and General Manager of the Advanced Networks Division at National Semiconductor Corporation, a semiconductor manufacturing company, where he worked from September 1992 to June 1994. Prior to joining National Semiconductor, Mr. Hart was a private consultant from February 1986 to September 1992 with Hart Weston International, a technology-based management consulting firm. Prior experience includes senior level management responsibilities in

21

semiconductor operations, engineering, sales and marketing with several companies including Motorola, Inc., an electronics provider, and National Semiconductor. Mr. Hart holds a B.S.E.E. degree from the University of Washington.

Andrew J. Pease will become our President effective March 30, 2009 and has served as our Vice President, Worldwide Sales since November 2006. From July 2003 to June 2006, Mr. Pease was Vice President of Worldwide Sales of Broadcom Corporation, a global leader in semiconductors for wired and wireless communications. From March 2000 to July 2003, Mr. Pease was Vice President of Sales at Syntricity, Inc., a company providing software and services to better manage semiconductor production yields and improve design-to-production processes. From 1984 to 1996, Mr. Pease served in a number of sales positions at Advanced Micro Devices, or AMD, a global semiconductor manufacturer, where his last assignment was Group Director, Worldwide Headquarters Sales and Operations. Mr. Pease previously held Vice President of Sales positions at Integrated Systems Inc., an embedded software manufacturer (1996-1997), and Vantis Corporation, a programmable logic subsidiary of AMD (1997-1999). Mr. Pease holds a B.S. degree from the United States Naval Academy and an M.S. in computer science from the Naval Postgraduate School in Monterey, California.

Terry L. Barrette joined QuickLogic in 1998 and has served as our Vice President, Operations since 2001 and Director of Manufacturing and Product Engineering since 1998. Prior to joining QuickLogic, Ms. Barrette was Director of Product Engineering and Manufacturing at GateField Corporation, a semiconductor manufacturer, from 1996 to 1998. Prior to joining GateField, Ms. Barrette was Manager of Test Engineering and Failure Analysis at LSI Logic from 1989 to 1996. Prior experience includes positions in product engineering, quality and reliability at GE Intersil, Intel and National Semiconductor. Ms. Barrette holds a B.S.E.E. degree from San Jose State University.

Ajith Dasari joined QuickLogic in July 2002 and has served as our Vice President of Worldwide Engineering since 2006, Senior Director of Engineering since 2005 and Director of Software Development since 2002. Prior to joining QuickLogic Mr. Dasari served in several product development positions from 1994 to 2002, most recently as the senior software manager in the Programmable System Level Integration group at Atmel Corporation, an advanced semiconductor manufacturing company. Prior experience includes a position in software development at Analogy, Inc., a developer of mixed signal simulation tools. Mr. Dasari holds a BSEE degree in electronics and communication from Nagarjuna University in India.

Brian Faith joined QuickLogic in June of 1996 and has served as our Vice President of Worldwide Marketing since November 2008. From 2001 through 2008, Mr. Faith served in various marketing positions including Vice President of Solutions Marketing and Senior Director of Marketing. Prior to 2001, Mr. Faith was an Engineering Program Manager, served in a Field Application Engineering role and held various Customer Application Engineering roles, including Customer Application Engineering Manager. Mr. Faith has also served as the Chairperson of the Marketing Committee for the CE-ATA Organization. He holds a B.S.C.E. degree in Computer Engineering from Santa Clara University and also served as Adjunct Lecturer at Santa Clara University for Programmable Logic courses.

Ralph S. Marimon has served as our Vice President, Finance and Chief Financial Officer since November 2008. Prior to joining the Company, Mr. Marimon served as Vice President, Finance and Operations, and Chief Financial Officer of Anchor Bay Technologies, Inc., a fabless semiconductor company that designs and produces advanced video processing chips from 2006. From 2005 to 2006, Mr. Marimon was Vice President of Finance and Administration and Chief Financial Officer of Tymphany Corporation, a provider of innovative audio transducers. Prior to that, Mr. Marimon was Vice President of Finance and Chief Financial Officer of Scientific Technologies, Inc., a provider of automation safeguarding products, from 2004 until 2005. From 1999 to 2003, he served at Com21 Corporation, a global supplier of system solutions for the broadband access market, where he was promoted from Corporate Controller to Vice President of Finance and Chief Financial Officer. Prior to

22

joining Com21 Corporation, Mr. Marimon was at KLA-Tencor Corporation for 11 years in a variety of senior executive financial management positions. Mr. Marimon began his career with National Semiconductor Corporation. Mr. Marimon holds a Masters of Management degree in finance and accounting from Northwestern University and a Bachelor of Arts degree in economics from the University of California, Los Angeles.

Catriona Meney joined QuickLogic in September 2003 and has served as our Vice President, Human Resources and Development since October 2006. Prior to joining QuickLogic, Ms. Meney was Vice President, International Human Resources at Ocular Sciences, Inc., a global manufacturer of contact lenses, from September 2001 to June 2002. In October 2000, Ms. Meney relocated to the United States. From May 1984 to October 2000, Ms. Meney held several human resource positions at Standard Life Assurance Co., an international financial services provider, located in Scotland, most recently as their Senior Human Resources Business Partner. Prior experience includes human resource positions at Sun Microsystems BV. Ms. Meney holds a M.A. degree, with honors, from the University of Glasgow in Scotland.

Timothy Saxe joined QuickLogic in May 2001 and has served as our Chief Technology Officer and Senior Vice President, Engineering since August 2006, and Vice President, Engineering since November 2001. From November 2000 to February 2001, Mr. Saxe was Vice President of FLASH Engineering at Actel Corporation, a semiconductor manufacturing company. Mr. Saxe joined GateField Corporation, a design verification tools and services company formerly known as Zycad, in June 1983 and was a founder of their semiconductor manufacturing division in 1993. Mr. Saxe became GateField's Chief Executive Officer in February 1999 and served in that capacity until GateField was acquired by Actel in November 2000. Mr. Saxe holds a B.S.E.E. degree from North Carolina State University, and an M.S.E.E. degree and a Ph.D. in electrical engineering from Stanford University.

Michael J. Callahan has served as a member of our Board of Directors since July 1997. From March 1990 through his semi-retirement in September 2000, Mr. Callahan served as Chairman of the Board, President and Chief Executive Officer of WaferScale Integration, Inc., a producer of peripheral integrated circuits. From 1978 to March 1990, Mr. Callahan held various positions at Monolithic Memories, Inc., a semiconductor manufacturing company, most recently as its President. During his tenure as President, Monolithic Memories became a subsidiary of Advanced Micro Devices, Inc., a semiconductor manufacturing company, where Mr. Callahan was Senior Vice President of Programmable Products. Prior to joining Monolithic Memories, he worked at Motorola Semiconductor for 16 years where he was Director of Research and Development as well as Director of Linear Operations. Mr. Callahan also serves on the boards of Micrel, Inc., a provider of analog power, mixed-signal and digital semiconductor devices, and Teknovus, Inc., a privately held company specializing in communications chipsets for subscriber access networks. Mr. Callahan holds a B.S.E.E. degree from the Massachusetts Institute of Technology.

Michael R. Farese has served as a member of our Board of Directors since April 2008. Mr. Farese is currently President and Chief Executive Officer and member of the Board of Directors of BitWave Semiconductor Inc., a fabless semiconductor company and innovator of programmable radio frequency ICs, a position he has held since September 2007. From September 2005 to September 2007, Mr. Farese was Senior Vice President, Engineering, of Palm, Inc., a leading mobile products company. He was President and Chief Executive Officer of WJ Communications, a radio frequency (RF) semiconductor company from March 2002 to July 2005 and President and CEO of Tropian, Inc., a developer of high efficiency RF ASICs for 2.5 and 3G cellular phones, from October 1999 to March 2002. Prior to that time, Mr. Farese held senior management positions at Motorola Corp., Ericsson Inc., Nokia Corp. and ITT Corp. Mr. Farese has held management positions at AT&T Corp. and Bell Laboratories, Inc. and has been in the telecommunications and semiconductor industry for more than 35 years. Mr. Farese holds a B.S. degree and a Ph.D in Electrical Engineering from Rensselaer Polytechnic Institute. He received his M.S. in Electrical Engineering from Princeton University.

23

Arturo Krueger has served as a member of our Board of Directors since September 2004. Mr. Krueger has more than 40 years of experience in systems architecture, semiconductor design and development, operations, and marketing as well as general management. Since February 2001, Mr. Krueger has been a consultant to automobile manufacturers and to semiconductor companies serving the automotive and telecommunication markets. Mr. Krueger was Corporate Vice President and General Manager of Motorola's Semiconductor Products Sector for Europe, Middle East and Africa from January 1998 until February 2001. Mr. Krueger was the Strategic and Technology/Systems advisor to the President of Motorola's Semiconductor Products Sector from 1996 until January 1998. In addition, Mr. Krueger was the Director of the Advanced Architectural and Design Automation Lab at Motorola. Mr. Krueger is a director of Marvell Technology Group Ltd., a semiconductor provider of high performance analog, mixed-signal, digital signal processing and embedded microprocessor integrated circuits, and NemeriX S.A., a provider of integrated circuits specializing in ultra low power RF and baseband chipsets for GPS and wireless applications. He holds an M.S. degree in Electrical Engineering from the Institute of Technology in Switzerland, and has studied Advanced Computer Science at the University of Minnesota.

Christine Russell has served as a member of our Board of Directors since June 2005. Since September 2008, Ms. Russell has been Executive Vice President of Business Development of Virage Logic Corporation, a provider of advanced intellectual property for the design of integrated circuits, where she previously served as Vice President and Chief Financial Officer from June 2006 to September 2008. Ms. Russell served as Senior Vice President and Chief Financial Officer of OuterBay Technologies, Inc., a privately held software company enabling information life cycle management for enterprise applications, from May 2005 until February 2006, when OuterBay was acquired by Hewlett-Packard Company. From October 2003 to May 2005, Ms. Russell served as the Chief Financial Officer of Ceva, Inc., a company specializing in semiconductor intellectual property offering digital signal processing cores and application software. From October 1997 to October 2003, Ms. Russell served as the Chief Financial Officer of Persistence Software, Inc., a company specializing in enterprise software providing infrastructure for distributed computing. Prior to 1997, Ms. Russell served in various senior financial management positions with a variety of technology companies for a period of more than twenty years. Ms. Russell formerly served as a director of Peak International Limited, a supplier of precision-engineered packaging products for storage, transportation and automated handling of high technology products, until Peak was acquired by S&G Company, Ltd. in June 2008. Ms. Russell holds a B.A. degree and an M.B.A. degree from the University of Santa Clara.

Hide L. Tanigami has served as a member of our Board of Directors since March 2007. Mr. Tanigami has served as the Chairman and Chief Executive Officer of Marubun/Arrow USA, LLC, a joint venture between Marubun Corporation, the largest semiconductor distributor in Japan, and Arrow Electronics since 1998. From 1994 through 1998, Mr. Tanigami was President and Chief Executive Officer of Marubun USA Corporation. From 1997 through 2000, Mr. Tanigami was the Chairman of Catalyst Semiconductor, Inc. and from October 1985 until March 1994, Mr. Tanigami was a co-founder and Vice President of Corporate Development at Catalyst Semiconductor, Inc. He has previously served on numerous boards in Silicon Valley, Japan and Taiwan. He currently serves on the board of directors of Marubun/Arrow and Ecrio, Inc., a developer of mobile phone communications and commerce software. Mr. Tanigami holds a B.A. degree from Kansai University of Foreign Studies and a M.A. degree from San Francisco State University.

Gary H. Tauss has served as a member of our Board of Directors since June 2002. From October 2006 to February 2008, Mr. Tauss served as President and Chief Executive Officer of Mobidia Technology, Inc., a provider of performance management software that enables wireless operators to provide users with high-quality mobile content. From May 2005 until the sale of its assets to Transaction Network Services, Inc. in March 2006, Mr. Tauss served as President, Chief Executive Officer and director of InfiniRoute Networks, Inc., a provider of software peering services for wireline

24

and wireless carriers. From October 2002 until April 2005, Mr. Tauss served as President and Chief Executive Officer of LongBoard, Inc., a company specializing in fixed-to-mobile convergence application software for leading carriers and service providers. From August 1998 until June 2002, Mr. Tauss was President, Chief Executive Officer and a director of TollBridge Technologies, Inc., a developer of voice-over-broadband products. Prior to co-founding TollBridge, Mr. Tauss was Vice President and General Manager of Ramp Networks, Inc., a provider of Internet security and broadband access products, with responsibility for engineering, customer support and marketing. Mr. Tauss earned both a B.S. and an M.B.A. degree at the University of Illinois.

Our CSSP design opportunities may not result in the revenue we expect

We have transitioned to becoming a supplier of CSSPs primarily to the mobile market from being a broad-based supplier of FPGA devices. We have developed a significant pipeline of design opportunities for CSSPs in our target markets and we are focused on converting these design opportunities into revenue. Revenue contributions from new mobile products will be important over the next two to four quarters in order to grow our business, achieve profitability and maintain or increase our cash and cash equivalent balances. Mobile product life cycles are short and we must replace revenue lost at the end of these product life cycles with sales from new design wins. In addition, we expect revenue from the rest of our business to decline due to the stage of our customers' product life cycles.